Have you ever wondered why your company’s financial statements don’t always match up perfectly with the money coming in and going out of your bank account? The answer often lies in the realm of accrual accounting, a system that recognizes revenues and expenses when they are earned or incurred, regardless of when cash is actually received or paid. One key aspect of accrual accounting is the concept of accrued expenses, and understanding how to record these expenses through adjusting entries is essential for accurate financial reporting.

Image: corporatefinanceinstitute.com

Accrued expenses represent expenses that have been incurred but not yet paid. Think of it like borrowing money from the future: you’re using a service or resource now, but the bill is coming later. For example, if your company receives electricity in December but doesn’t pay for it until January, you have an accrued expense for electricity in December. Accrued expenses are crucial because they ensure that your financial statements accurately reflect the costs of doing business during a specific period, regardless of when those costs are settled.

Understanding the Mechanics of the Adjusting Entry

The adjusting entry to record an accrued expense is a fundamental concept in accounting. It involves two key accounts: the expense account itself and a liability account called “Accrued Expenses.” The adjusting entry increases the expense account, reflecting the cost of the service or resource consumed, and increases the liability account, representing the company’s obligation to pay for that expense.

Debits and Credits: The Foundation of Accounting

To understand the adjusting entry, it’s essential to grasp the fundamental principles of double-entry bookkeeping. Every accounting transaction affects at least two accounts, one with a debit and one with a credit. Debits increase asset and expense accounts and decrease liability, equity, and revenue accounts. Credits do the opposite; they decrease asset and expense accounts and increase liability, equity, and revenue accounts. This system ensures that the accounting equation (Assets = Liabilities + Equity) always balances.

The Mechanics of the Adjusting Entry: A Concrete Example

Let’s imagine your company receives $500 worth of utilities in December but won’t pay the bill until January. The adjusting entry to record this accrued expense would look like this:

- Debit: Utilities Expense – $500

- Credit: Accrued Expenses – $500

This entry increases the Utilities Expense account by $500, reflecting the cost of the utilities consumed in December. It also increases the Accrued Expenses liability account by $500, representing the company’s obligation to pay the utility bill in January.

Image: learn.financestrategists.com

The Importance of Accrued Expense Adjustments

Failing to record accrued expenses has significant implications for your financial statements. Here’s why:

1. Understated Expenses:

Not recording accrued expenses results in understated expenses on the income statement. This misrepresents the true cost of doing business during the period, leading to an artificially inflated profit figure.

2. Overstated Net Income:

An understated expense, in turn, leads to an overstated net income, potentially misleading stakeholders about the company’s financial performance.

3. Inaccurate Balance Sheet:

The balance sheet is a snapshot of a company’s assets, liabilities, and equity at a specific point in time. Not recording accrued expenses results in an inaccurate balance sheet, understating liabilities and overstating equity.

4. Difficulty in Making Informed Decisions:

Misleading financial statements can lead to poor decision-making by management, investors, and creditors. They may rely on inaccurate information, leading to unwise investments, financing decisions, or operational strategies.

5. Compliance with Accounting Standards:

Accrual accounting is a cornerstone of Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS). Failing to record accrued expenses violates these standards and may result in financial penalties or other legal consequences.

Beyond the Basics: Common Accrued Expenses and Their Implications

Accrued expenses are not limited to electricity bills. They encompass a wide range of expenses that businesses encounter regularly, including:

1. Salaries and Wages:

Accrued salaries and wages represent payments due to employees for work already performed but not yet paid. This often occurs when a company’s pay cycle does not align with the end of the accounting period. For example, if the company’s pay day is the first Friday of the month, and the accounting period ends at the end of the month, there will be a portion of employee wages accrued.

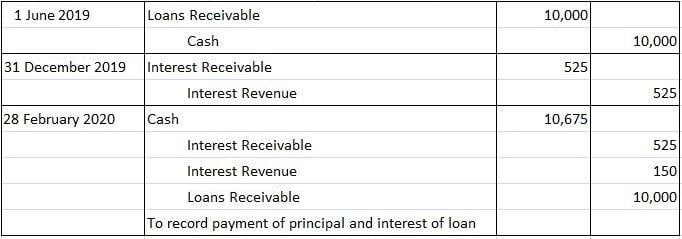

2. Interest Expense:

Interest expense accrues on loans or other debt instruments. Even when the interest payment is not due until a later date, the company must record the interest cost incurred during the accounting period.

3. Rent Expense:

When a company leases property, rent expense accrues on a pro-rata basis over the lease period. Even if the monthly rent payment is made at the beginning of the month, the company must record the portion of the rent that relates to the days within the accounting period.

4. Property Taxes:

Property taxes are often paid in arrears, meaning they are collected in the year following the year in which they apply. The company must accrue the property tax expense in the period it is incurred (the year the property tax is applicable), even if the payment is made in the following year.

5. Depreciation:

Depreciation expense represents the decline in value of long-term assets (such as equipment, buildings, and vehicles). This expense is usually accrued evenly over the asset’s useful life, regardless of whether any cash payments are made.

The Adjusting Entry To Record An Accrued Expense Is

The Importance of Timely and Accurate Accrual Accounting

Accrued expense adjustments are essential for accurate financial reporting. They ensure that the financial statements reflect the true cost of doing business during a particular period, allowing for sound decision-making and compliance with accounting standards.

Understanding the adjusting entries to record accrued expenses is critical for anyone involved in accounting or finance, from company executives to investors. It’s vital to invest the time and effort to master this fundamental concept, ensuring that your financial statements paint an accurate picture of your company’s performance.

Do you have any questions about recording accrued expenses or other accounting adjustments? We encourage you to share your thoughts and experiences in the comments below! Your insights can be valuable to others.

")

")